Triple-market architecture

How spot, perpetuals, and prediction markets work together on 1024EX and what cross-market strategies they enable.

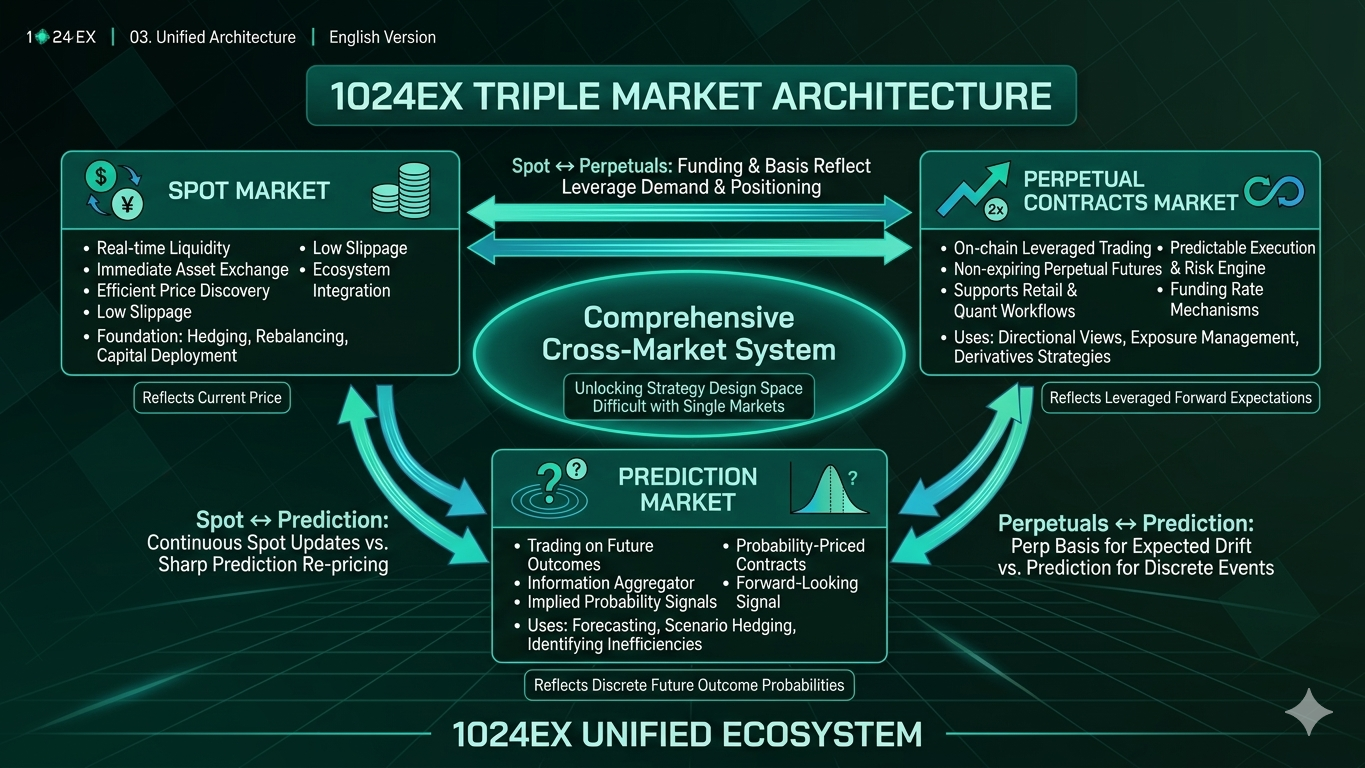

Spot Market

The spot market on 1024EX provides real-time liquidity for immediate asset exchange. It is designed for efficient price discovery, low slippage, and tight integration with the rest of the 1024 ecosystem. Spot trading is the foundation for hedging, rebalancing, and capital deployment.

Perpetual Contracts Market

The perpetual contracts market enables on-chain leveraged trading via non-expiring perpetual futures. It supports both retail and quantitative workflows with predictable execution, a risk engine, and funding-rate mechanisms. Perpetuals are used to express directional views, manage exposure, and build derivatives-driven strategies that pair naturally with spot and prediction markets.

Prediction Market

The prediction market enables trading on future outcomes using probability-priced contracts. These markets aggregate information into an implied probability, providing a forward-looking signal that complements traditional price markets. Prediction contracts can be used for forecasting, scenario hedging, and identifying cross-market inefficiencies.

Using all three markets together

The strength of 1024EX comes from treating spot, perpetuals, and prediction markets as one unified architecture. Each market reflects a different dimension of expectations:

Combining these markets lets you compare current price, leveraged positioning, and event probability in one view. That makes it easier to spot mispricing, hedge defined scenarios, and design strategies that rely on more than one signal.

- Spot reflects the current price.

- Perpetuals reflect leveraged forward expectations through basis and funding.

- Prediction markets reflect the probability of discrete future outcomes.

Together, these layers support strategies that a single market cannot support on its own.

Cross-market pricing relationships

Because each market processes information differently, prices do not always move in perfect alignment. These gaps can form actionable signals:

- Spot ↔ Perpetuals: funding and basis reflect leverage demand and positioning.

- Spot ↔ Prediction: spot prices update continuously, while prediction probabilities can reprice sharply on new information.

- Perpetuals ↔ Prediction: perp basis reflects expected drift, while prediction contracts price discrete event probabilities.

You can monitor these discrepancies and trade them systematically.

How the three markets interact on 1024EX

On 1024EX, the connection between spot, perpetuals, and 1024EX Predict is not just conceptual — it is operational. These markets can be observed side by side, interpreted together, and acted on within one native environment.

A move in spot can reset the reference price for perpetuals. A change in perp basis or funding can reveal leverage demand and directional crowding. A repricing in 1024EX Predict can surface event-driven expectations before they are fully expressed in continuous price markets. When read together, these markets provide a richer picture of both current conditions and forward expectations.

This is where the design of 1024EX becomes especially powerful. Users are not forced to treat each market as an isolated venue. Instead, they can move from signal to hedge, from hedge to expression, and from expression to strategy refinement in a more connected workflow. A trader may use spot for inventory, perpetuals for tactical exposure, and 1024EX Predict for event-sensitive positioning. A quant or agent-driven workflow can monitor all three layers simultaneously, detect divergence, and convert that divergence into structured execution logic.

In practice, this creates a system where price, leverage, and probability are continuously informing one another. Rather than asking only “Where is the market now?”, users can also ask “What is the market pricing next?”, “How crowded is that view?”, and “Is there a mismatch between implied probability and tradable price?”. That broader decision surface is what makes cross-market trading on 1024EX strategically distinct.

Example strategy categories

1. Mispricing arbitrage (spot + prediction, or perp + prediction)

When prediction-implied probabilities diverge from what spot or perps imply, traders can construct low-risk or delta-neutral structures:

- Buy underpriced prediction contracts.

- Hedge directional exposure using spot or perpetuals.

- Capture convergence as pricing normalizes.

Best for: event-driven traders, market-neutral funds, automated execution systems.

2. Basis and probability spread trading

Perpetuals often trade at a premium or discount (basis) relative to spot due to funding dynamics. Prediction contracts may imply a different forward expectation.

Common structures include:

- Long perp / short prediction when basis implies stronger drift than outcome probability.

- Long prediction / short perp when probability implies more upside than perps price.

This expresses a spread between forward expectations (probability) and leveraged expectations (basis/funding).

3. Scenario hedging and tail protection

Prediction contracts can hedge specific thresholds or states (for example, “BTC above 60k by Friday”). Traders can overlay prediction positions onto spot or perp portfolios to:

- Hedge tail risks tied to defined scenarios.

- Add conditional exposure that only pays off if the event occurs.

- Reduce downside while maintaining core positioning.

This can serve as a practical alternative to options-style payoff shaping for discrete outcomes (where markets exist and resolution rules are clear).

4. Leveraged outcome amplification

By combining:

- Spot for base exposure,

- Perpetuals for adjustable leverage,

- Prediction contracts for event-driven multipliers,

traders can create payoff curves similar to structured products:

- Digital-like payoffs,

- Range-style expectations,

- Conditional leverage that activates only if a scenario occurs.

5. Tri-market statistical arbitrage

Quant systems can continuously observe:

- Spot microstructure and mid-price deviations,

- Perp funding and basis shifts,

- Prediction probability updates.

Common approaches include:

- Cross-market mean reversion,

- Lead-lag detection (prediction markets may reprice faster on certain news),

- Volatility and regime inference using probability drift.

This category is well suited for systematic research and automated execution.

6. Liquidity and execution optimization

Liquidity conditions vary by market. Traders can:

- Enter exposure in the most liquid venue (often spot or perps),

- Hedge or express conditional views using prediction contracts,

- Rebalance dynamically as implied probabilities and basis shift.

This approach can reduce market impact while improving informational efficiency in execution.

Why the triple-market architecture matters

Integrating spot, perpetuals, and prediction markets creates a multi-layer trading environment that is:

- Rich in signals (price, basis/funding, probability)

- Deep in liquidity (multiple venues for expressing views)

- Diverse in payoff structures (continuous and discrete outcomes)

- Naturally suited for algorithmic and quantitative strategies

This turns 1024EX into a full-spectrum market system for trading, hedging, and research workflows that benefit from cross-market interactions.

FAQ

- Why does 1024EX offer spot, perpetuals, and 1024EX Predict together?

Because each market captures a different part of market belief. Spot captures current price, perpetuals capture leveraged forward positioning, and 1024EX Predict captures the market-implied probability of discrete future outcomes. Together, they create a more complete view than any single market alone. - What is the main advantage of using all three markets together?

The main advantage is context. A price move in spot may look straightforward on its own, but when combined with perp funding, basis, and event probabilities, it can be interpreted much more precisely. This helps users identify whether a move is driven by spot demand, leveraged positioning, event repricing, or a combination of all three. - How can these markets be used in one strategy?

A user might hold spot as core exposure, use perpetuals to increase or reduce directional risk, and use 1024EX Predict to express or hedge a specific event view. More advanced workflows can systematically scan for misalignment across price, funding, basis, and implied probabilities. - Why do prices across the three markets sometimes diverge?

Because they process information differently. Spot is continuous and inventory-driven. Perpetuals are influenced by leverage demand, positioning pressure, and funding mechanics. 1024EX Predict prices discrete outcomes and can reprice sharply when new information changes the odds of a specific event. These structural differences naturally create temporary gaps. - Is cross-market trading only for advanced users?

No. Basic users can still benefit by using the three markets as informational layers, even without running complex strategies. For example, a user may look at spot for price, perp funding for crowding, and 1024EX Predict for event sentiment before making a decision. More advanced users can go further and formalize these relationships into systematic strategies. - How does AgentX fit into this workflow?

AgentX can help users interpret information across all three markets, surface relevant signals, and translate those signals into actionable strategy logic. Instead of manually switching between disconnected views, users can monitor price, leverage, and probability as one linked system and make decisions with a clearer execution path. - Are cross-market discrepancies always tradable?

Not always. Some discrepancies reflect real differences in time horizon, liquidity, event structure, or market participation. A gap is only useful if it is large enough, durable enough, and executable enough to overcome costs and risk. The goal is not to assume every mismatch is alpha, but to identify the ones that matter. - What risks should users keep in mind?

Users should consider execution risk, liquidity differences, funding cost, slippage, event-resolution uncertainty, and timing mismatch between markets. Cross-market strategies can be powerful, but they work best when the relationship being traded is clearly defined and risk is controlled from the start.

Updated 2 months ago